Approximately 90% of China’s steel mills use blast furnace-basic oxygen furnaces and iron ore to produce steel. Moreover, most steel mills are fuelled by coal, so the sector accounts for an outsized share of China’s carbon emissions.

China could reduce its carbon footprint by switching its steel mills to electric arc furnaces (EAFs), which use steel scrap rather than iron ore. About 10% of China’s steel output is from EAFs, but there has been minimal progress in recent years despite the otherwise rapid transition to green technology in other parts of the economy. A relative lack of steel scrap within China explains some of the reluctance (more mature economies have larger amounts of steel scrap), alongside the fact that most steel mills in China are not nearing the end of their life. The current average age of steel mills in the country is just 12 years, according to the commodities research company Wood Mackenzie. Moreover, industrial players and some provincial governments expressed concerns that a large EAF steel sector would place too much pressure on the electricity grid.

An unprecedented surge in iron-ore demand

China is a major producer of iron ore, accounting for around 30% of global supply (as of 2024), but it also imports to meet its needs, not least because domestic iron ore is typically low grade and often high cost to produce. Chinese demand has driven massive production growth in Australia and Brazil. Australia’s iron ore output rose from 267m tn in 2000 to 970m tn in 2024. Iron ore is now Australia’s largest export by value and Brazil’s second largest, after soybeans. Five companies – Australia’s BHP, Fortescue, Hancock Prospecting and Rio Tinto, and Brazil’s Vale – account for 75–80% of annual exports, with China taking around 75% of global imports.

Such is the scale of the trade in iron ore to China that a new type of cargo ship, the very large ore carrier (VLOC or Valemax ships), was developed specifically to travel the long distance from Brazil to China. (Iron ore by its nature is a large volume commodity, so transport in small ships is a costly option.) The five aforementioned companies are particularly vulnerable to any downturn in China’s steel production or in its use of blast furnaces to make steel.

Despite its dominance in the iron-ore trade, China has often complained that the five external mining companies operate as a cartel. In 2022, the China Mineral Resources Group was created to centralise the purchase of iron ore in an effort by China to take more control over prices. In September, there were unconfirmed reports that China had banned iron-ore shipments from Australia’s BHP Group after price talks with China’s group had broken down. With new sources of supply coming online, it appears that China feels it is in a stronger position to exert influence in the market.

One new entrant in particular is expected to have a big impact. The Simandou project in Guinea is scheduled to come online this year and could eventually account for around 5% of global supply. There has been major investment in the project by Chinese companies, but Rio Tinto and the Guinea government also hold stakes. It will produce a very high grade of iron ore, which will make it popular with steel mills seeking to curb emissions.

More recent developments

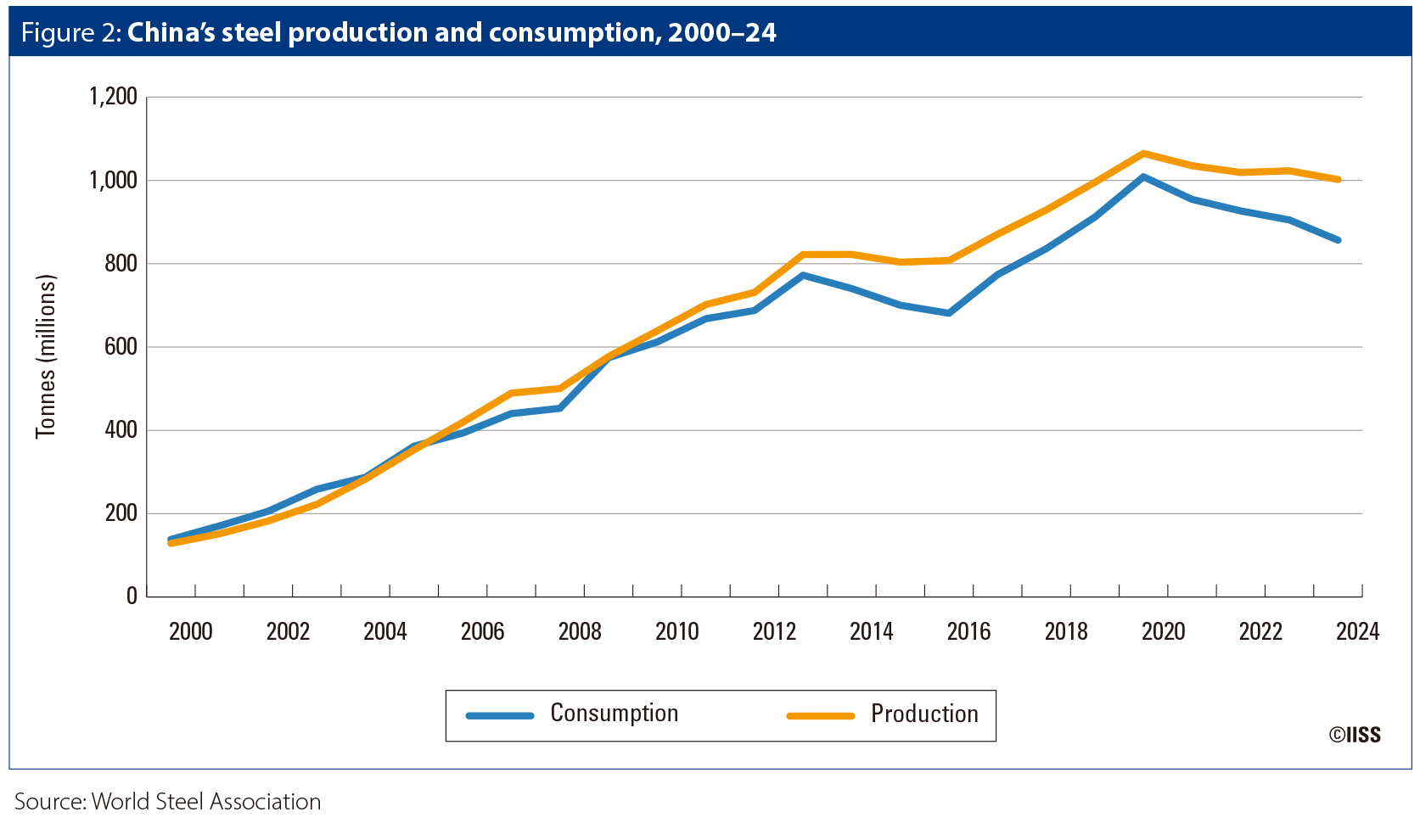

China’s apparent steel use (estimated based on production minus exports and change in stocks) peaked in 2020 at 1bn tn, according to the World Steel Association, but fell to 857m tn by 2024. A further fall looks likely in 2025. The ongoing downturn in China’s real-estate construction sector explains most of this decrease. Steel demand from the auto sector and from green-energy technology (electric vehicles and wind turbines, for example) has been increasing, but these sectors are growing from a much lower base.

Steel production also peaked in 2020 and in September 2025 was down 4.6% year-on-year. Given that production has not fallen by as much as consumption, oversupply has remained a feature of the market.

China’s steel exports surged in 2024, reflecting the domestic oversupply, particularly to markets in Southeast Asia. Export volumes reached 110m tn last year, compared with the more typical 75m tn of annual exports. It was widely suspected that Chinese steel was being repackaged and sent abroad as an export from Southeast Asia in a bid to circumvent sanctions on Chinese steel – a practice that has likely taken place to varying degrees for years, increasing sharply in 2024 but easing in 2025. The increase in exports last year prompted a raft of protectionist steps from a diverse set of countries in both the developed and developing world. Data from the price-reporting agency Platts and the China Iron and Steel Association show that in the year to February 2025, 29 steel-trade cases were filed against China, compared to only 15 in 2020–23. Regardless, crude-steel exports were still up by a further 9.2% year-on-year in the first nine months of 2025. It seems likely, however, that exports could start to drift lower in the coming months and into 2026 as trade restrictions bite.

This is particularly the case since in October the European Commission announced that the EU’s tariff on steel would double to 50%. It also cut duty-free import quotas by 47% to 18.3m tn. The EU’s latest move is probably a response to the hike in the US tariff on steel to 50% earlier this year. European steel producers were concerned that with high-tariff barriers in the US, low-cost producers would flood the European market.

Given the fall in steel production this year, iron-ore imports have arguably held up well, decreasing by just 0.1% year-on-year in January–September. That said, stocks at Chinese ports have been falling, which has been a factor supporting iron-ore prices.

Outlook

Given that the Chinese economy is likely to continue to transition away from infrastructure-led growth, domestic steel use will remain in decline. The persistent fall in domestic demand is unlikely to be offset by increased exports, so the oversupply in the market could expand in the next few years. Eventually the combination of weaker demand and lower prices (reflecting the oversupply) should force producers to curtail output, though this will probably be a slow process given the state’s reluctance to jeopardise employment.

“Eventually the combination of weaker demand and lower prices … should force producers to curtail output, though this will probably be a slow process given the state’s reluctance to jeopardise employment.”

Nonetheless, over the next few years, China’s iron-ore imports are expected to start to fall. This may be compounded by the fact that the government has set unofficial targets of EAF production accounting for 15% of total output in 2025 and 20% by 2030. Although the 2025 target will not be met, there could be more progress between now and 2030. More steel scrap is being generated in China as it has now been over 20 years since the building boom began and properties do not have as long of a shelf life in China as they do in Europe, for example. The government has also created the China Resources Recycling Group to promote scrap recycling. The electricity grid is expanding rapidly and is increasingly fuelled by renewable energy, so the EAF’s emissions will be markedly lower.

There are also greater financial incentives to move to EAF production in the form of carbon prices and taxes. The current carbon price in China, which was recently extended to cover the steel sector as well as power plants, is currently too low to deter coal-based steel production, but this could change. The EU’s proposed Carbon Border Adjustment Mechanism – an effective tax on carbon content scheduled to come into effect in 2026 – could also be avoided if China offered EAF-made steel.

The combination of lower absolute production and increased output from EAFs will probably lead to a marked decline in China’s iron-ore imports. Consolidation in the iron-ore sector is expected as a result, with the closure of some higher-cost capacity. Australia’s ore grades are starting to decline, which will make the country’s iron ore less competitive, and it will command a lower price. (High-grade ore reduces the amount of coking coal needed to produce steel and is generally a more efficient, less polluting option.)

“The combination of lower absolute production and increased output from [electric arc furnaces] will probably lead to a marked decline in China’s iron-ore imports.”

It is not all bad news for the world’s iron-ore producers. India has ambitious plans to increase its steel production and is one of the few countries where production is currently rising. It grew by 8% in 2024 and was up by 10.2% year-on-year in January–August this year. The government is targeting annual output of 300m tn by 2030, up from nearly 200m tn in 2024. But India is the fourth-largest iron-ore producer in the world, has large reserves and is a net exporter. It may be the case that it will start to import more iron ore in the coming years, but it is unlikely to offset falling Chinese imports. Southeast Asian economies, notably Indonesia, Malaysia and Vietnam, are also planning to raise steel output and would need to import iron ore. However, given the lack of local inputs, EAF production is being encouraged.

If, as is expected, China’s overall steel production declines, and EAF production rises, the iron-ore market will move into a large surplus and prices will fall. Consolidation in the industry is likely and there will be financial pressure to close higher-cost or low-grade mines. That said, government support might be forthcoming for some smaller producers outside of Australia and Brazil as steel (and its inputs) has in the past been seen as a strategic sector.

|